One agent tells you the market is picking up; another says deals have dried up completely. The thing is, they're both right. That's the most accurate description of where Canadian housing actually is right now – prices aren’t collapsing, but they’re not meaningfully rising, either. Sales volumes are weak. New construction is both booming and stalling, depending on where you look. Policy is trying to stimulate demand at the exact same time macro conditions are suppressing it. If you've been trying to identify a single narrative about this market, bullish or bearish, that's probably why nothing seems to make sense.

Demand has changed, not just declined.

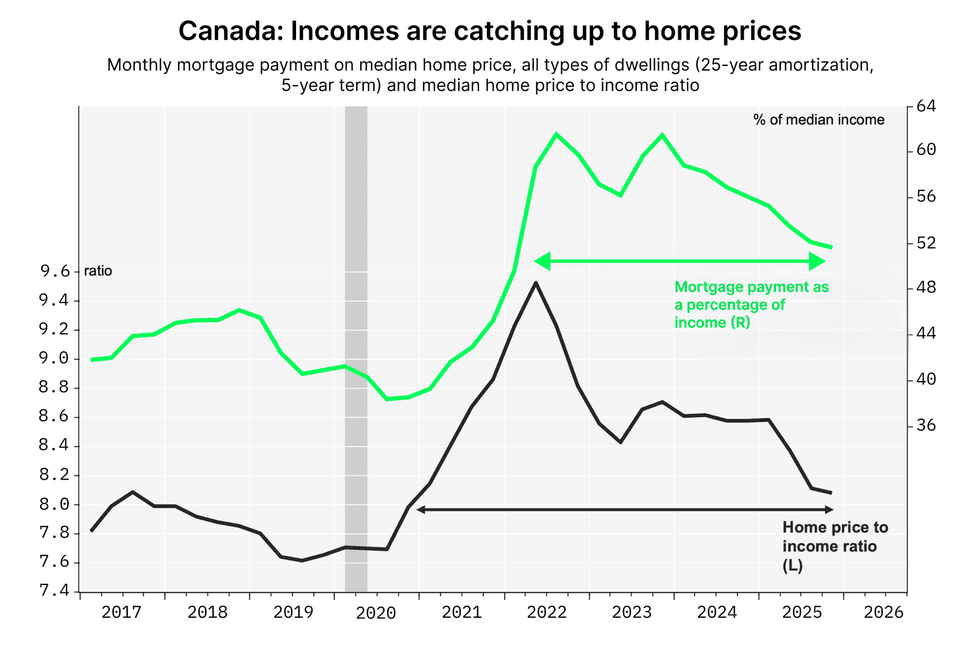

Higher interest rates reduced affordability and also froze the market in place. First-time buyers are hitting qualification limits, move-up buyers are locked into low-rate mortgages they don’t want to give up, and investors, who drove a significant share of activity in the last cycle, are now staring at negative cash flow in most major markets. Rate cuts have helped, but not as much as people were hoping. Instead of overall price, buyers often think in terms of what's coming out of their bank accounts each month, and those numbers are still painful.

NBC Economics and Strategy (data via Statistics Canada, Teranet-National Bank, CREA)

National Bank

Transaction volumes tell the same story: They remain well below historical norms, even in markets where prices appear relatively stable. That's not a sign of equilibrium, it's a standoff – sellers aren't dropping prices, buyers can't qualify for what sellers are asking, so transactions just aren't happening. It’s a quieter market, sure, but not necessarily a cheaper one.

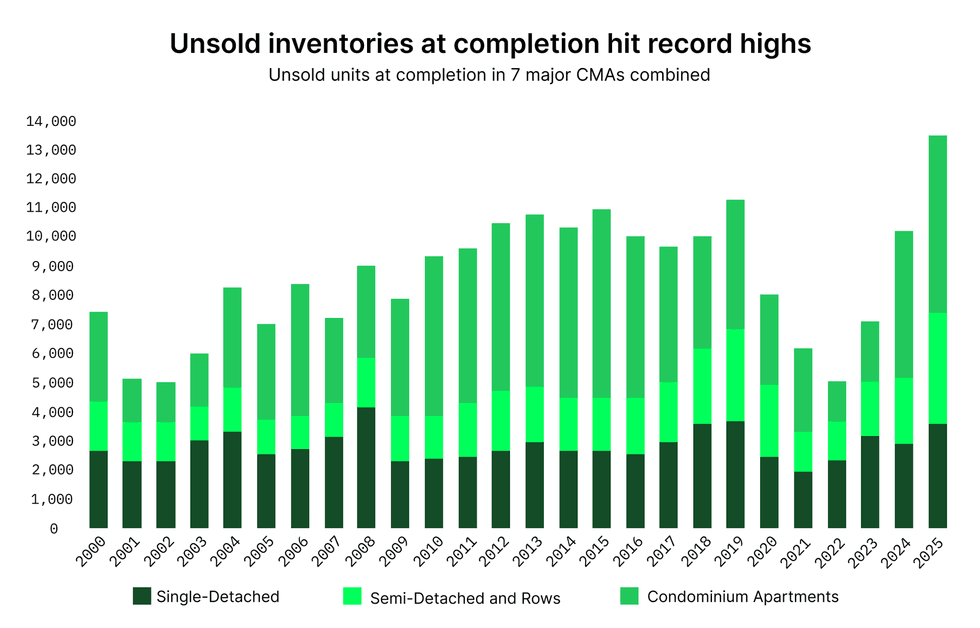

Supply is showing up, just not where it's needed

All those pre-construction condos sold in 2020 and 2021 are finishing now and landing on the market at once. Purpose-built rental is expanding, helped along by government incentives. Low-rise housing is a different story, still boxed in by zoning rules, construction costs, and the fact that there just isn't much land left to build on.

This isn't broad oversupply. It's concentrated, and where it's concentrated matters. Small, investor-oriented condos in major urban markets are seeing the most pressure, while family-oriented housing remains relatively tight.

CMHC

Recent policy moves, specifically the HST and GST rebates on new construction, are designed to stimulate demand and help absorb that incoming supply. In theory, they lower prices and improve project viability, but in practice, the impact is less clean. The rebate is largely aimed at the wrong buyer: pre-construction condos are mostly sold to investors, not first-time buyers, so the policy doesn't move the needle for those who actually need it. And even for buyers who do qualify, a third of new homes sold in Toronto last year were priced above the $1 million threshold for the full rebate.

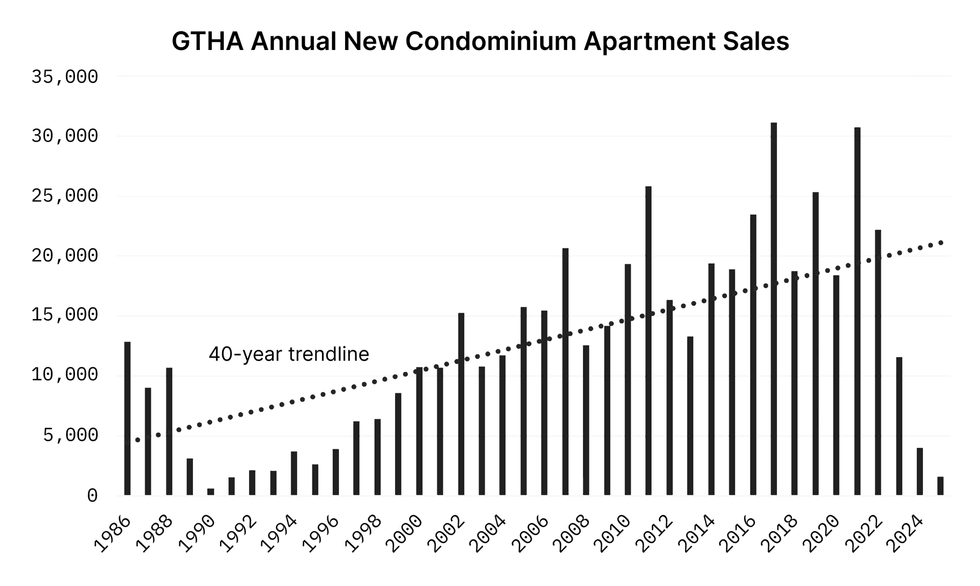

New construction demand doesn't materialize out of nowhere, either. A lot of it comes at the expense of resale. This is where the idea of “filtering” is useful: When someone buys a new unit, they typically vacate an existing one, which becomes available to someone else, usually at a lower price point. In a healthy market, this creates a chain of transactions that distributes supply more efficiently, but that chain can break. If move-up buyers hesitate or financing becomes restrictive at any point in the ladder, inventory starts to accumulate in specific segments.

Urbanation

The population backstop is weaker than the bull case assumes

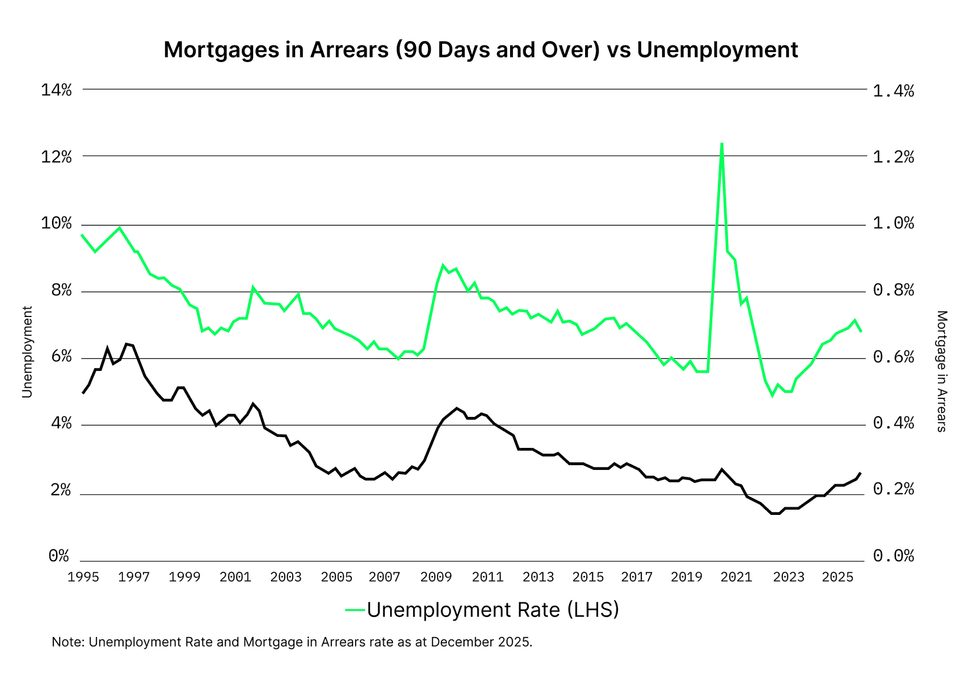

A lot of the bullish narrative still leans on population growth – and over the long term, that argument holds. In the short term, though, that backstop is weaker than people are giving it credit for. Population growth is slowing. Non-permanent resident policies are tightening. And at the same time, unemployment is beginning to rise in key urban markets.

Housing demand isn’t just about how many people there are. It’s about how many people can actually afford to buy or rent. Mortgage renewals are the slow-moving part of this story that hasn't fully arrived yet. A large cohort of borrowers who locked in ultra-low rates during the pandemic will be renewing into a much higher rate environment over the next couple of years. Early data from the Canada Mortgage and Housing Corporation is already showing rising delinquencies in more stretched markets like Ontario. A sharp correction isn't inevitable, but the stress is building.

Canadian Bankers Association

Two markets, same address

At the entry level, demand is holding up. These are people who need to live somewhere, often with help from family money. In the investor-heavy end of the market, particularly small urban condos, the dynamics are very different. Those buyers are running the numbers on interest rates, rent income, and what it costs to carry the unit every month. That's why the market feels so inconsistent.

Something else is happening underneath all of this that doesn't get much attention. AI is starting to drive down the cost of closing a deal, from mortgage underwriting to marketing to administrative workflows. I've been watching this from inside the industry, through the AI-agent tools we're building for realtors at meetyourhomies.com and the deal analysis platform I helped develop for listeners of the Canadian Real Estate Investor Podcast at Realist.ca. The easy assumption is that AI spells bad news for anyone in a junior role, but what I'm actually seeing is more output, with the industry adjusting around the new tools.

Where this goes from here

The divergence will likely deepen. Entry-level housing will probably hold up. The condo investor segment is a different story, and new construction is going to keep competing directly with resale in a way it hasn't before. Prices aren't likely to crater, but they're not skyrocketing, either.The long-term case hasn't changed: Canada keeps growing and housing supply is still constrained. But the macro isn't going to tell you much about what's actually happening right now. The variables that do matter are the granular ones: what you're buying, where, at what price, and how you're financing it.