When Susan Harvey took ownership of her parents’ house in the Algonquin Highlands in 2010 – first as a cottage, then as her primary home in 2014 – she also inherited something else: a sister who hasn’t spoken to her since.

“We were happy to buy her out so she could buy a house,” says Harvey, a retired interior designer. “She felt the process took too long and that I was trying to cheat her. It was a very difficult time that was totally unexpected.”

Harvey, now in her 70s, admits she does have worries about what’s best as far as leaving her home to her children, who are in their 30s and 40s and live in B.C., Ontario, and Ireland. “I’m not sure that any of them would end up living here,” she says. “In the end, it might be a non-issue.”

Harvey isn’t alone in facing the question of what happens next. Across Ontario and B.C., the median age of multiple-property owners is now 60-something and counting. So, as Canada’s baby boomers and older Gen Xers age out, their much-loved vacation homes are presumably going to wind up in the hands of their kids or grandkids.

But inheriting a cottage comes with some serious baggage far beyond the potential family drama.

“Parents always have good intentions,” says Thuy Lam, an advice-only financial planner with Objective Financial Planners based in Markham, Ont. “They kind of underestimate the ongoing cost [of owning a cottage] because they may be in a good financial position themselves – especially the boomer generation – and they’ve built up a good nest egg.”

Because even if the mortgage is paid off, the bills aren’t. Property taxes, insurance, utilities, maintenance, repairs – it all adds up. Property taxes alone on a $627,700 cottage – the median price of a single-family recreational home in Canada – could range from $1,952 to $12,759 a year, depending on your postal code. And cottage insurance is usually more expensive than a regular home, because cottages sit empty more and are farther away from fire stations.

Harvey backs this up. “We did initially think it would be cheaper to live at the cottage,” she says. “Our taxes rose faster and more than expected.” Plus, trees don't chop themselves, snow doesn't plow itself, and cottage groceries aren't cheap.

If the heirs to these cottages are millennials and Gen Z, their average salary is no higher than $63,000 a year. That’s not a cottage budget; that’s a “maybe I can pay rent this month” budget. Even if they could afford it, Lam says a lot of clients choose to avoid the ongoing cottage bills altogether, instead spending that money on sunny vacations or simply renting a cottage for a few weeks in the summer.

If the heirs to these cottages are millennials and Gen Z, their average salary is no higher than $63,000 a year. That’s not a cottage budget; that’s a “maybe I can pay rent this month” budget.

Some people try to split the difference, renting out the cottage to offset the costs. Maryrose Coleman, senior vice president of sales at Sotheby's International Realty Canada and owner of a cottage rental agency, says this is increasingly common. "We often end up with clients on the rental side because they're trying to offset the quite high expense of maintaining a cottage that they've inherited from their parents," she says.

Owners will rent it out for part of the summer and use it themselves the rest of the time. It's a way to keep the property without drowning in bills, but it only works if you can handle being a landlord on top of everything else.

Even if you can afford the carrying costs, there's a bigger problem: taxes. When you inherit property in Canada, the CRA treats it as if the previous owner sold it at fair-market value. If that property has increased in value, capital gains tax applies.

But there’s an exception: the primary residence exemption. If you sell the home you actually live in, the government does not tax you on the profit. It’s basically the CRA saying, “This was a home, not a financial side hustle.” A cottage can qualify for this exemption too, but only for the years it was officially your primary residence. If your parents owned it for 30 years but only lived there full-time for the last five, you’re only protected from tax on those five years. For the other 25? Capital gains tax applies – and yes, paying that bill can be painful.

Assuming you have to pay capital gains tax, here’s the fun (ahem, not fun) part: in Canada, 50% of your capital gains count as taxable income, which then gets taxed at your regular rate. So, if a cottage was bought for $200,000 and later left to someone at a $900,000 fair-market value, that’s a $700,000 gain – and half of that is taxable. Translation: that could mean a $90,000 to $100,000 tax bill, depending on income and what province you live in.

Lam admits this “can become a little bit of a nightmare,” especially when one heir gets the cottage and another gets the rest of the estate. The person who inherited the cottage doesn't pay the capital gains tax, the estate does, which means the other heir is stuck with the bill.

All of the ongoing costs and tax implications get even messier when the cottage is left to more than one person and expenses have to be shared. “Usually, one kid lives close or enjoys the cottage and another one just doesn’t use it as often,” says Lam. “What’s the fairness and what’s the split?” As a result, sometimes, the best plan is a “for sale” sign.

Coleman has seen this play out. "We did a sale a couple of years back where there were five siblings, three of whom didn't want to keep the family cottage and two of them who did," she says. "So that's always challenging because there's going to be two people who are disappointed, because the other siblings will override and the property ends up getting sold and they no longer have access to what was a cherished family cottage."

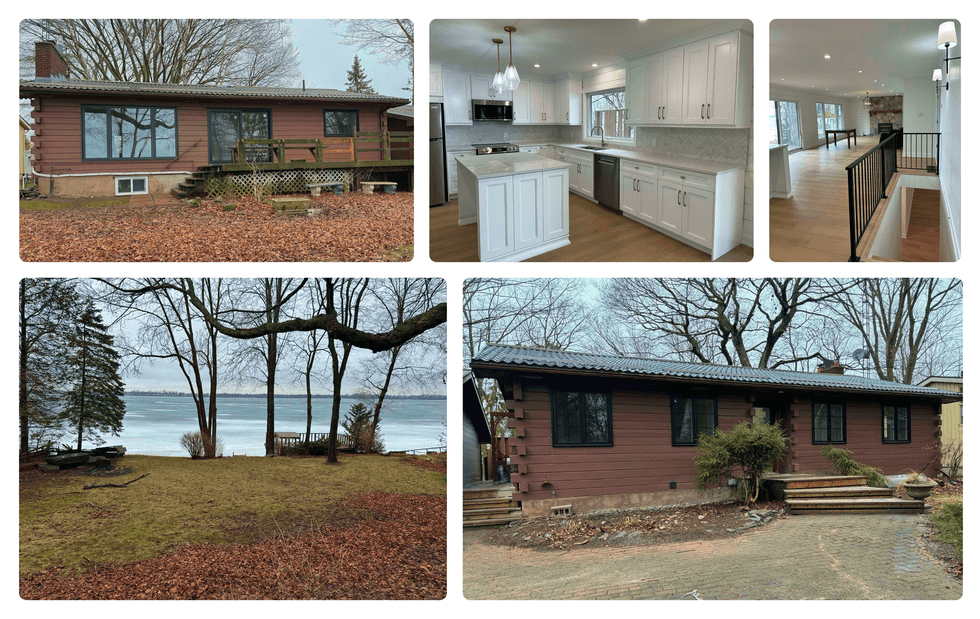

Andrew Harkness, a 43-year-old from Georgetown, Ont., thinks he's found a way through.

In 2025, he and his wife bought a cottage in Prince Edward County on West Lake for $1.075 million – with his parents. “We couldn’t really get it on our own, it was a bit too much money,” he says. “But joining our resources made it attainable.”

The property is currently under renovation, but when the dust settles, it will be his parents’ full-time home, while Harkness, his wife, and their sons will use it as their vacation cottage. His parents own the majority of the home on the title, and their plan is to will their ownership directly to Andrew’s children.

Why skip Andrew and his wife? Two reasons: probate and taxes.

Andrew Harkness co-owns the family cottage with his parents, who will leave their share to Andrew's children. Andrew Harkness

Andrew Harkness co-owns the family cottage with his parents, who will leave their share to Andrew's children. Andrew Harkness

Because the ownership structure was set up this way from the start, the grandparents’ share will pass directly to the grandkids without getting stuck in probate. And because Andrew and his wife own a home plus part of the cottage, inheriting more of it would likely trigger capital gains tax on what the CRA would consider a secondary property.

But if it goes straight to the grandkids, who don’t own property yet, the cottage could potentially qualify as their primary residence down the line. According to Lam, this only works because the ownership has been structured properly from day one (ideally with an estate lawyer’s help) and because the cottage is the grandparents’ primary residence now.

Talk to your inheritors now. Find out whether they want the cottage and whether they can handle the carrying costs. If the answer to both is yes, start planning for the tax hit.

Lam adds that people often assume they can dodge probate and capital gains tax by just putting their kids on the title. But that only works if the ownership structure is genuine from the beginning (like with the Harkness family) – not just slapped on later. “Changing the names on the deed doesn’t necessarily mean you’ve changed who ‘owns’ the property for tax purposes,” she says. “In many cases, the CRA will treat the original owner(s) as still being the beneficial owner.” Because the grandparents are original owners and it’s their primary residence, they’re able to skip some of the tax headaches.

Of course, Harkness’ creative approach hinges on a very specific set of circumstances: living parents willing and able to co-buy a million-dollar property. Most Canadians don't have that option, which is why selling while you're alive, paying the capital gains tax yourself, and passing on the proceeds can sometimes make more financial sense. Or maybe the best thing you can leave your kids is the permission to sell, and the best inheritance is the financial freedom to make their own choices.

If you do want to keep it in the family though, Lam's advice is simple: Talk to your inheritors now. Find out whether they want the cottage and whether they can handle the carrying costs. If the answer to both is yes, start planning for the tax hit – whether that means setting aside liquid assets or taking out a life insurance policy to cover it.

Harkness has simpler advice: call in the pros. “Go get expert advice from accountants or real estate lawyers,” he says. “It's money well spent.”

Even when selling is clearly the right financial move, Coleman warns it's rarely as clean as people expect. "People are often surprised about how upset they get after it's sold," she says. "They might have thought they were fine and they've moved forward and they're selling, and then all of a sudden it hits them: the property's sold, and they hadn't really processed it. There's a real grief that happens, especially with a cottage."

Canada’s cottage landscape is headed for a generational reset: Some will be sold off and others will sit vacant, casualties of an affordability crisis that's made cottage life a luxury most people can't touch.

For most other people? They’ll inherit the cottage dream, all right – and the financial nightmare that comes with it.