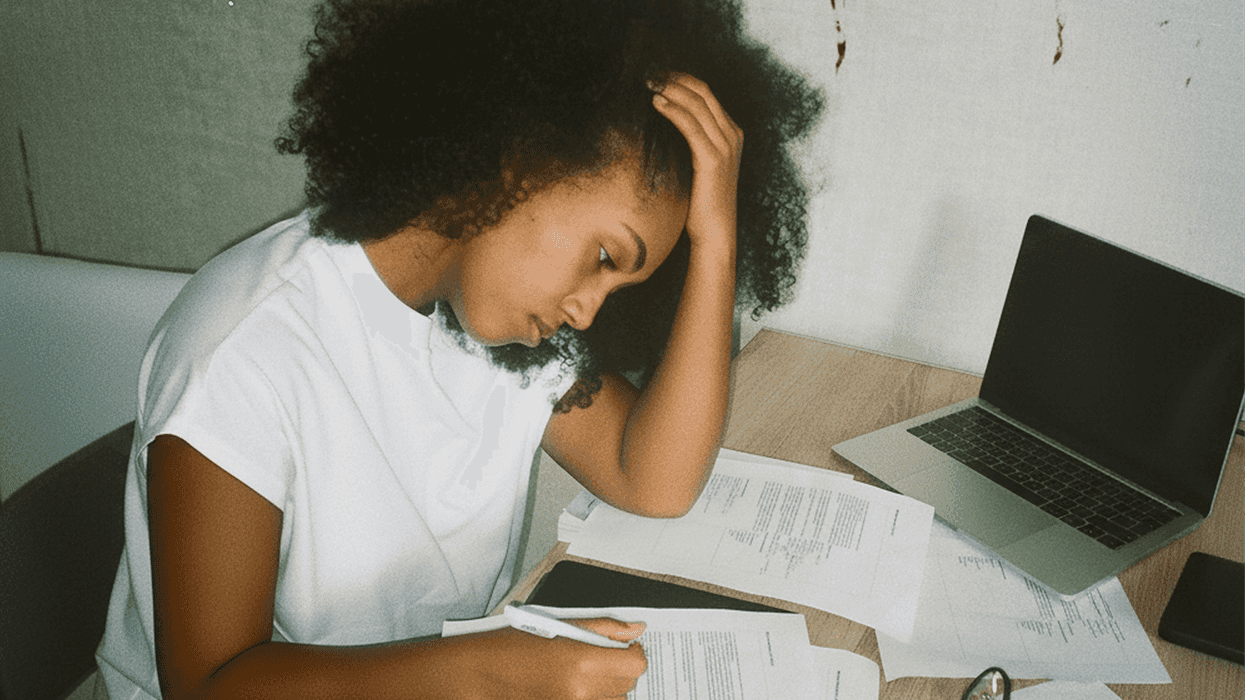

Inside a No Frills on Lansdowne Avenue in Toronto, Sarah Thompson* stood in the dairy aisle, staring at a carton of eggs. She had just sent $400 to her cousin for quote-unquote "car repairs" (one of multiple e-transfers she’d made to family members recently) and was now doing some familiar calculations in her head: would the money left over in her account be enough to cover both her own groceries and her rising condo fees?

The 34-year-old senior project manager earns a six-figure salary.

“I actually started to feel sick,” Sarah says. “I’m thinking, I make over a hundred thousand dollars a year. Why am I panicking over a dozen eggs?”

*A pseudonym she requested due to the social stigma around discussing family financial dynamics in her community.

Sarah is paying the loyalty tax, the informal, compounding cost of being the most financially capable person in the family. In an economic climate where families are increasingly struggling and the household-debt-to-income ratio has climbed to more than 177%, the "stable child" often becomes the safety net – not by choice, but by proximity. What their family sees as mandatory or expected generosity from the stable child is, in reality, preventing that child from growing their own wealth or preparing for retirement.

The process was supposed to be straightforward: work hard, climb the ladder, and secure your future. But for a specific class of high-achievers, that came with extra fees they weren’t prepared for: "loans" to family that never got paid back, a parent's mortgage that somehow turned into a shared expense, and relatives who called to say “remember where you came from.” Most stable children don’t even register paying the loyalty tax as a choice.

The identity trap

For people unfamiliar with it, this kind of family dynamic feels strange and confusing. Why don't they simply say no? Well, the requests rarely arrive as demands but as emergencies, temporary situations, or passive-aggressive hints. A repair bill here, a rent payment there – and they’re for beloved family members, why wouldn’t you help them? By the time the pattern’s noticeable, the expectations have already been set, and the consequences of defying them can go beyond just their bank account.

"When family needs arise, it does not feel like a financial decision. It feels like a test of who you are," says Vanessa Bowen, a chartered professional accountant and founder of the financial coaching company Mint Worthy Co. As she sees it, the loyalty tax often comes into play when a person's financial growth starts to outpace their emotional conditioning around money, where their financial situation looks strong on paper, but they’re carrying an identity where they were told to be responsible and help others. "When support is driven by guilt rather than intention . . . it creates an unsustainable pressure that leads to a quiet erosion of wealth."

The requests rarely arrive as demands but as emergencies, temporary situations, or passive-aggressive hints. A repair bill here, a rent payment there – and they’re for beloved family members, why wouldn’t you help them?

Plus, saying "no" doesn't actually end the request for money, it just changes the form of the request. The next stages could involve higher-pressure tactics like labelling them "selfish" for the refusal, sending other family members to convince them, giving the silent treatment for extended periods, excluding them from important events, or worse. So on paper, the professional is doing incredibly well, but internally, they’re still carrying the identity they've been conditioned to perform: the family member taught to be responsible for others, to never complain, and to never outshine.

When you grow up with this treatment and have internalized your family's expectations, saying "no" is hard – and each successive "no" gets exponentially harder. Whether it’s a son feeling the weight of a father’s failed pension or a daughter managing a sibling’s debt, family needs (or "needs") come up and it feels more dire than just a bank withdrawal – to deny it feels like betrayal, both of your family and of your own self. The high achiever is caught in a loop where their financial success is viewed as a communal asset and their financial anxiety is treated as a personal failing.The cost of keeping quiet

Sarah is the embodiment of this trap. Despite the impressive salary and a condo near Liberty Village, she remains anchored to a secret ledger she can't share with her peers. In her professional circles, admitting that your family is your biggest financial liability is a social taboo, so to her coworkers, she’s the senior project manager who "has it all." To her family, though, she’s the relative who "forgot where she came from" if she even hesitates on the next Interac transfer.

People often think success is a ladder, but to me, it feels more like a treadmill where the incline keeps rising.

For Sarah, the loyalty tax is more than an abstract figure – it's the $80,000 she's funnelled into family "emergencies" over the last five years. Nobody sees the high-interest credit card debt she's accumulating to cover their "emergencies" because she's too ashamed to admit that her six-figure salary is being stretched across three different households. While her colleagues discuss property values and diversified portfolios, Sarah stays quiet, knowing that a significant portion of her wealth has already been spent on lives other than her own.

"People often think success is a ladder, but [to me,] it feels more like a treadmill where the incline keeps rising," she says. "Every time I get a raise, a new 'emergency' pops up back home. I’m not building wealth; I’m subsidizing a lifestyle for my relatives that I can’t even afford for myself. I am the insurance policy my parents never bought and the retirement fund everyone else didn't save for."

Unforgiving math

We often frame $400 here or $1,000 there as just "help." Run the numbers, though, and those small gestures start looking catastrophic.

"You aren't just giving away cash; you're trading your 70-year-old self’s security for a relative's immediate crisis," says Alim Dhanji, a Senior Financial Planner with CI Assante Wealth Management in Vancouver, B.C. He estimates that if the $80,000 Sarah "gifted" were invested instead, it would have grown to roughly $615,000 over a 35-year career. "By compromising your own baseline today, you eventually lose the capacity to help anyone, including yourself, in the future."

In more tangible terms, the national home price is forecast to rise to roughly $689,000 in 2026. Sarah’s $80,000 "gift" is a down payment on a home she will never own.

Building a financial firewall

Surviving the loyalty tax requires more than a budget. The Canadian financial system is designed around the assumption that your money is yours alone, but for a significant portion of the population, it isn’t, really, and it never has been. The guilt you feel when you don't give is the penalty being levied, and recognizing that is what makes intentional decision-making possible.

Dhanji's suggestion is to use the mechanics of the Canadian system to create what he calls a "technical no." He recommends setting aside a maximum of $5,000 annually for family needs, as well as putting core assets in accounts like RRSPs that are not easily accessible. By moving those assets into less accessible accounts, the barrier becomes legal rather than emotional.

"Telling a relative the money is locked in isn't just an excuse; it's a protection against a 30% withholding tax," Dhanji says. "It shifts the conversation from your willingness to help to the mathematical reality of the account itself. You aren't saying 'I won't help you'; you are saying, 'the system will penalize me 30% for touching this.' It turns the bank into the bad guy, allowing you to preserve your family relationship while protecting your baseline."

The missing reckoning

For a generation of Canadians like Sarah, this problem isn't a failure of willpower or financial literacy. The familial conditioning that makes "no" feel like treachery started long before the first e-transfer request ever came.

The loyalty tax remains a private struggle because the industry that was built to "help" – the advisors, the banks, the policymakers – has likely never had to reckon with it. Until that changes, the people paying the loyalty tax will keep paying it in lost compound interest, in delayed retirements, and in checking a bank balance in a grocery aisle while earning six figures. The system will keep calling them a success story, but they'll know better.